Blockchain has the potential to revolutionize how gold and precious metals are manufactured and delivered.

Consider the journey a gold nugget must take along its supply chain, from mine to end consumer—it cuts through several other industries and practices, including legal, regulatory, financial, manufacturing and retail, each of which might have its own ledger system.

These ledgers are vulnerable to hacking, fraud, errors and misinterpretations. They can be forged, for example, to conceal how the metal or mineral was sourced.

With blockchain technology, there’s no hiding anything. Decentralization guarantees complete transparency, meaning anyone along the supply chain can see how, when and where the metal was produced, and who was involved every step of the way.

This will give the industry a huge shot of trust, not to mention dramatically increase efficiency.

Many producers, tech firms and entire jurisdictions have already adopted, or plan to adopt, blockchain technology for these very reasons. IAMGOLD, a Toronto-based producer, announced last month that it partnered with Tradewind Markets, a fintech firm that uses blockchain technology to facilitate digital gold trading. IBM just helped launch a diamond and jewelry blockchain consortium, TrustChain, that will track and authenticate diamonds, metals and jewelry from all over the world. And sometime this year, the Democratic Republic of Congo will begin tracking cobalt supply from mines to ensure children were not involved.

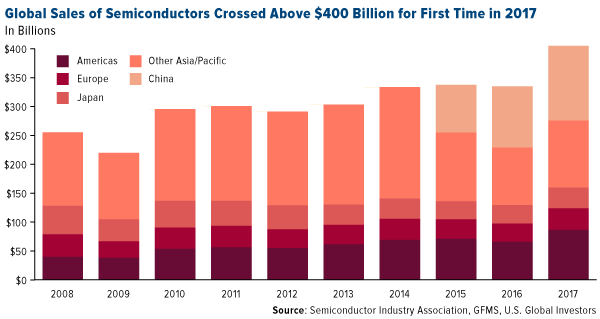

With precious metals being used more widely in industrial applications, from smartphones to electric cars to Internet of Things (IoT) appliances, tracking metals across the supply chain has become increasingly more important to businesses and consumers. According to the Semiconductor Industry Association (SIA), global sales of semiconductors—which contain various metals, including gold—crossed above $400 billion for the first time in 2017. Total sales were $412.2 billion, an increase of nearly 22 percent from the previous year.

That’s a lot of metal and other materials that blockchain tech can help authenticate.

Apart from this, blockchain is also bringing change to gold investment. Consider Royal Mint Gold (RMG), which aims to provide the “performance of the London Gold Market with the transparency of an exchange-traded security.” There’s also the Perth Mint’s InfiniGold, which issues digital certificates guaranteeing ownership of gold and silver in the mint’s vault. A number of other platforms exist to help facilitate gold trading.

Should even one of these become hugely popular, it “could be as big a change to the gold markets as the development of ETFs, but with the added advantage of appealing to younger generations,” according to the World Gold Council’s (WGC) chief strategist, John Reade.

To Conclude

Blockchain has many advantages and usecases apart from being just a payment method or as a store of value (well, not exactly the common store you’d find though with its extreme volatitity, but for those who bought Bitcoin for example when it was just $100s of dollars and sold it when went up to$19,000 late last year, to them I refer).

There are many other industries which require high levels of trust and transparency which Blockchain technology can solve. Yes, we are in the early stages of the tech and just like any new tech or trend, it does take time to iron out the shortcomings and improvise for the mass markets to adopt.

What is your opinion on Blockchain being used for other precious metals manufacturing apart from Gold?

Article partially curated from USfunds.com.

Image courtesy of USfunds.com & Wikimedia